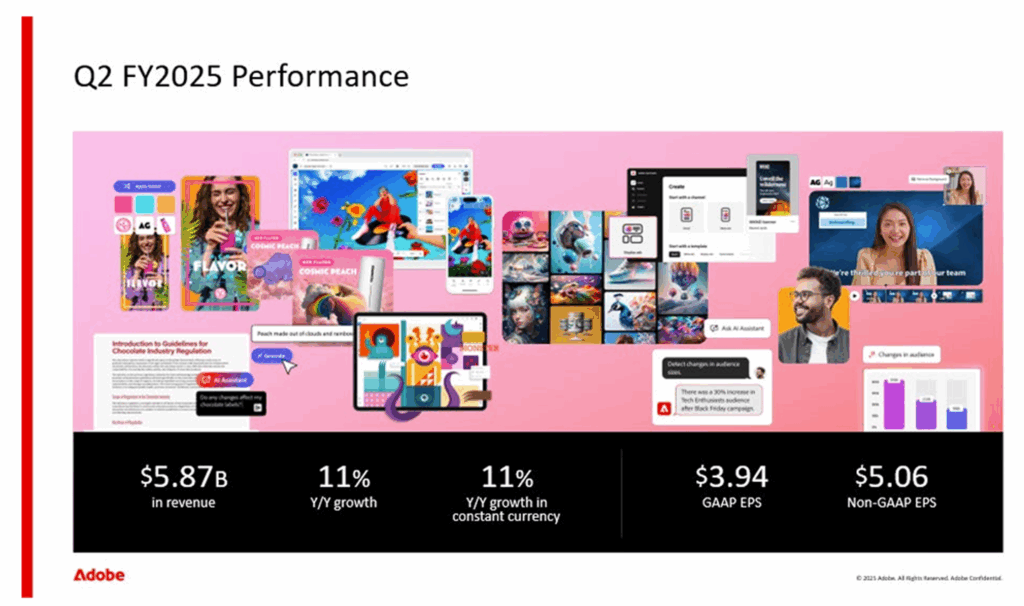

On June 12, 2025, Adobe Inc. reported financial results for its second quarter fiscal year (FY) 2025 ended May 30, 2025. The company notched record revenue in the quarter and raised its FY2025 revenue and earnings per share (EPS) targets.

However, the stock cannot catch a break from the market’s bears, and all the blame is attributed to the potential disruption that artificial intelligence (AI) may cause to Adobe’s business.

This post delves into the latest earnings release, separating the signal from the noise and ascertaining what the quarter’s performance means for Adobe’s bull and bear theses.

Adobe Inc.: What Problem Does It Solve?

Adobe Inc. is a leading American global software company known for its creative multimedia products. Founded in 1982, Adobe revolutionized digital content creation with groundbreaking software like Photoshop (image editing and graphic design), Illustrator (vector graphics editing), Premiere Pro (video editing), and Acrobat (creating, managing, and manipulating PDF files).

Adobe pioneered digital document management with its creation of the ubiquitous PDF format. Through its Creative Cloud suite, Adobe enables individuals and organizations to design, edit, and share visual content with ease.

Headquartered in San Jose, California, Adobe continues to drive innovation in digital media, marketing solutions, and cloud-based services, shaping the way people interact with creativity and information worldwide.

Adobe’s Business Segments: How It Makes Money

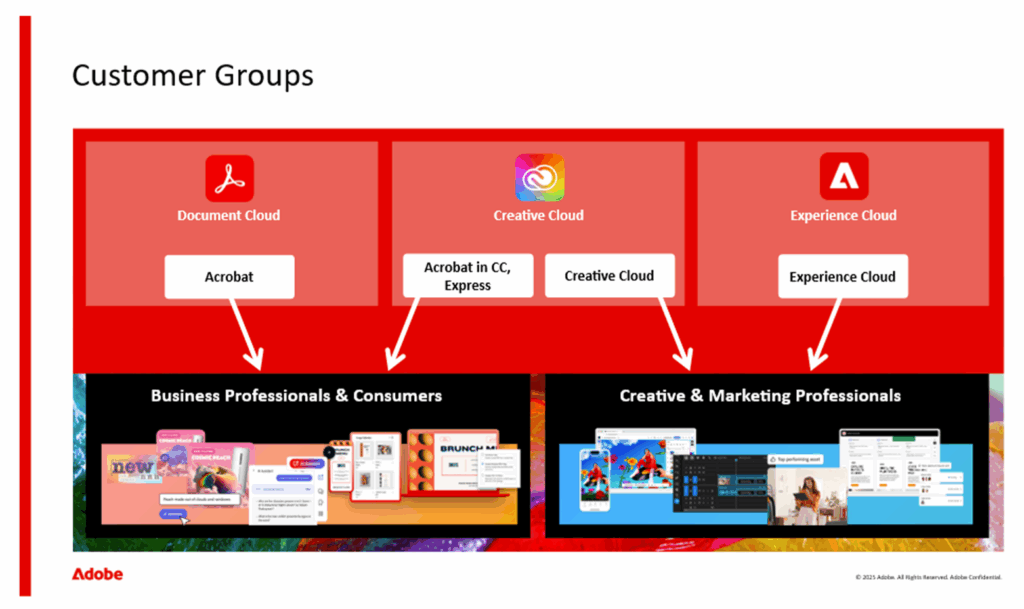

Adobe Inc. is more than a software company; it is a multifaceted innovator at the crossroads of creativity, business, and technology. Its business segments – Digital Media, Digital Experience, and Publishing and Advertising – are synergistic pillars that drive growth, diversification, and resilience.

1. Digital Media

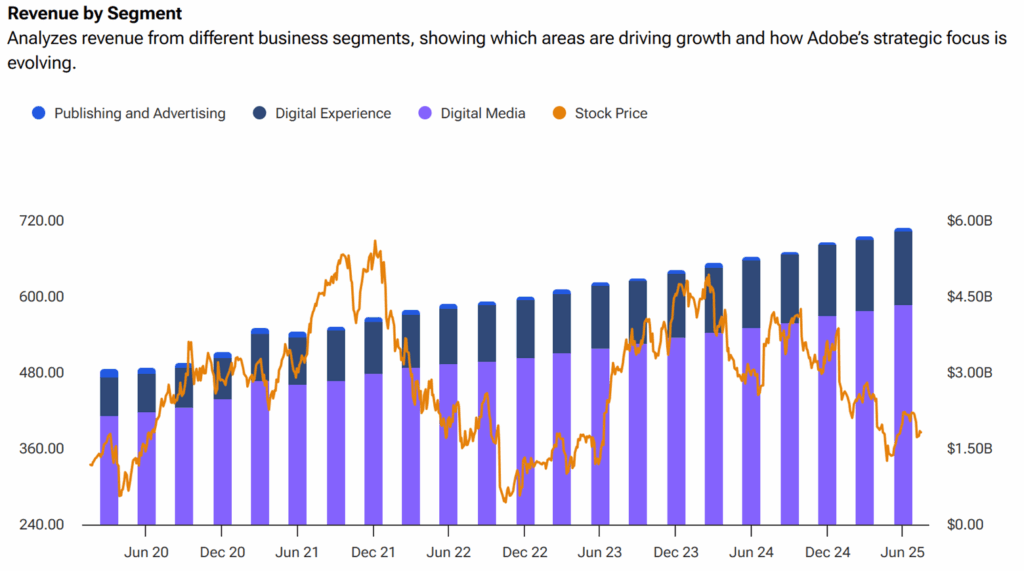

At the heart of Adobe’s operations lies the Digital Media segment, a powerhouse that encompasses the company’s renowned creative tools and services, used worldwide by artists, designers, videographers, photographers, and other creative professionals. It consistently generates over 70% of Adobe’s annual revenue (74% in Q2 FY2025) and comprises Adobe’s Creative Cloud and Document Cloud product suites.

Creative Cloud

Creative Cloud is the beating heart of the Digital Media segment. It offers a subscription-based model for a comprehensive suite of applications, including industry standards such as Photoshop, Illustrator, InDesign, Premiere Pro, After Effects, and more. These tools allow users to create, edit, and publish content across multiple media – from graphics and photographs to videos and interactive experiences.

The subscription model ensures continuous updates and improvement, with cloud connectivity enabling collaboration, file sharing, and access to assets from virtually anywhere. Creative Cloud’s influence extends to educational institutions, agencies, and enterprises, making it an essential part of the modern creative workflow.

Document Cloud

Document Cloud represents Adobe’s foray into digital document management and workflow automation. Central to this segment is Adobe Acrobat, which enables users to create, edit, sign, and manage PDF documents. Together with Adobe Sign, a leading e-signature solution, Document Cloud empowers businesses and individuals to streamline paper-based processes, improve productivity, and enhance security.

The PDF, invented by Adobe, remains the global standard for reliable, cross-platform document exchange. Document Cloud leverages this ubiquity, integrating AI and cloud-driven features to create more intelligent and efficient document workflows. It caters to sectors ranging from legal and finance to education and government.

2. Digital Experience

As the world’s economy continues to shift further towards the digital realm, Adobe’s Digital Experience segment has emerged as a key driver of growth. This segment delivers enterprise solutions designed to transform how businesses engage with their customers across digital channels. It consistently generates about 25% of Adobe’s annual revenue and comprises Adobe’s Experience Cloud product suite.

Adobe Experience Cloud

The Adobe Experience Cloud is a comprehensive suite for marketing, analytics, advertising, and commerce. It empowers organizations to deliver personalized customer journeys and manage content, campaigns, and data with intelligence and agility.

- Adobe GenStudio for Performance Marketing: A generative AI-first application that lets marketing teams create their own ads and emails to drive impactful, personalized marketing campaigns.

- Adobe Experience Manager (AEM) Sites: A leading content management system (CMS) enabling businesses to build, manage, and optimize digital experiences across websites, mobile apps, and other channels.

- Adobe Experience Manager Assets: A customizable digital asset management system (DAM) that lets businesses easily discover, govern, and activate millions of assets to deliver and scale personalized experiences.

- Adobe Analytics: Provides deep insights into customer behaviour, enabling data-driven decisions to increase engagement and drive conversion.

- Adobe Target: Offers robust testing and personalization capabilities, allowing businesses to deliver tailored content and experience based on real-time data.

- Adobe Campaign: Facilitates the orchestration and automation of personalized, cross-channel marketing campaigns.

- Adobe Commerce: A robust e-commerce platform that integrates with the Experience Cloud, empowering businesses to build and scale online stores.

These solutions, often powered by artificial intelligence through Adobe Sensei, help enterprises optimize their marketing efforts, personalize user experiences, and gain actionable insights in a hyper-competitive digital marketplace. The Digital Experience segment serves clients across various sectors, including retail, banking, travel, and media, that value customer experience as a key differentiator.

3. Publishing and Advertising

While Digital Media and Digital Experience represent Adobe’s primary growth engines (accounting for 99% of revenues), the company also maintains a segment focused on legacy products and niche solutions – the Publishing and Advertising segment.

Legacy Publishing Solutions

Adobe’s roots in publishing run deep, tracing back to the invention of PostScript, a page description language that revolutionized desktop publishing. Today, Adobe continues to support traditional publishing with products like FrameMaker for long-form technical documentation and Adobe RoboHelp for help authoring. These tools, though not as prominent as Creative Cloud, remain vital in industries that rely on sophisticated document workflows.

Advertising Solutions

Adobe’s advertising tools complement its marketing technologies. Adobe Advertising Cloud enables agencies and brands to manage, automate, and optimize digital advertising campaigns across channels, including search, display, video, and social. The platform harnesses data and AI to drive targeted, effective ad placements and maximize return on investment.

4. Emerging Technologies and Strategic Initiatives

Innovation is woven into the fabric of Adobe’s identity. Beyond its established segments, Adobe invests in emerging technologies and strategic initiatives that promise future growth.

Artificial Intelligence – Adobe Sensei

Adobe Sensei is the company’s unified AI and machine learning framework. Embedded across product lines, Sensei powers intelligent features such as auto-tagging images, automating repetitive tasks, and offering predictive analytics. These capabilities not only enhance the user experience but also keep Adobe’s offerings at the forefront.

Cloud Integration and Platform Expansion

Adobe’s cloud-native strategy enables seamless integration between its various clouds (Creative, Document, and Experience) and fosters interoperability with third-party services. This approach ensures that Adobe remains relevant in enterprise IT environments and continues to evolve in response to customer needs.

Mobile and Web-based Solutions

Recognizing the shift to mobile and browser-based workflows, Adobe has developed lightweight, accessible versions of its flagship applications. Products like Adobe Spark and mobile variants of Photoshop and Illustrator enable creative productivity from virtually any device.

Adobe’s Q2 FY2025 Earnings Report Highlights

Adobe posted a record revenue of $5.87 billion, an 11% increase from the same period last year:

- GAAP (Generally Accepted Accounting Principles) earnings per share for the quarter stood at $3.94, while non-GAAP earnings per share reached $5.06, demonstrating a year-over-year (YoY) growth of 13%.

- Cash flows from operations of $2.19 billion, which is a record for Q2 (suggesting its 13% fall compared to the previous quarter was primarily due to seasonal reasons).

- At the end of the quarter, Remaining Performance Obligations (RPO) were $19.69 billion, representing a 10% YoY increase (or 11% in constant currency). Current Remaining Performance Obligations (cRPO) also grew 10%, both as reported and in constant currency.

- The AI book of business, encompassing AI-first products such as Acrobat AI Assistant, Firefly App and Services, and GenStudio for Performance Marketing, is currently on track to exceed the $250 million annual recurring revenue (ARR) target by the end of fiscal year 2025.

Remaining Performance Obligations (RPO) is a financial metric that denotes the total monetary value of revenue yet to be realized by a company from its contracts. This metric represents the unfulfilled portions of these contracts and highlights potential future revenue streams. RPO is particularly relevant to SaaS and subscription-based businesses, where contractual agreements typically span multiple periods.

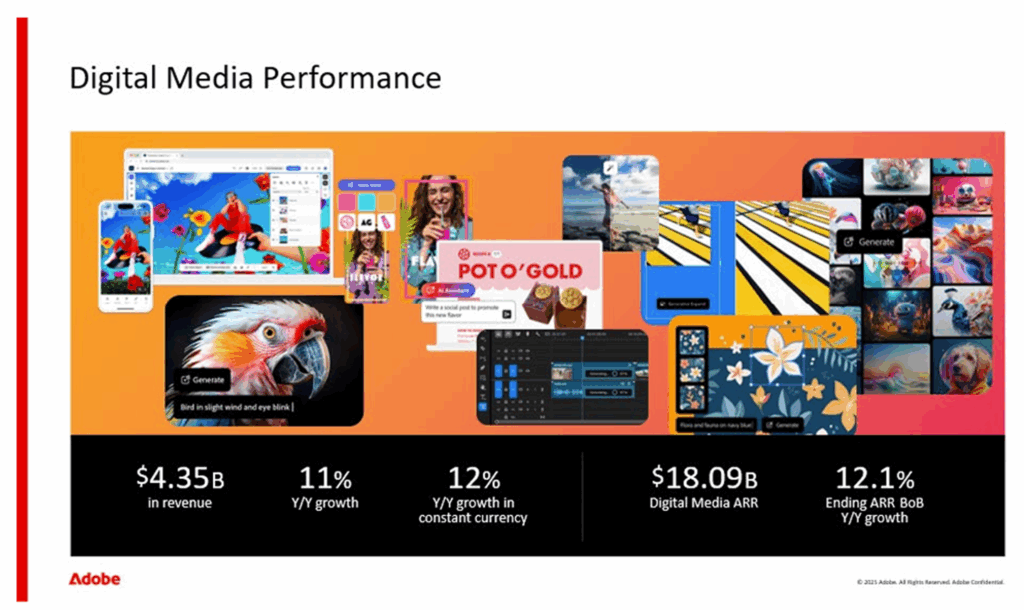

Digital Media’s revenue increased 12% to $4.35 billion YoY. Digital Media ended the quarter with $18.09 billion in ARR, a 12.1% YoY increase. Subscription revenue for Digital Media’s Business Professionals and Consumers Group grew 15% YoY:

- Adobe now has over 700 million monthly active users (MAUs) across its family of Acrobat and Express products, representing a YoY increase of over 25%.

- Approximately 300% quarter over quarter (QoQ) and 1100% YoY increase in the adoption of Express capabilities within Acrobat.

- Over 75% YoY increase in students gaining access to Acrobat AI Assistant and/or Express Premium plans.

- Over 35,000 new businesses added Adobe’s family of Acrobat and Express products in the second quarter. Express alone added around 8,000 new businesses this quarter, about 600% growth YoY (including companies such as Microsoft, ServiceNow, Workday, Intuit and top sports leagues like MLB, the NFL, and Premier League).

Adobe has rolled out new Firefly offerings globally and will deliver more innovation over the next few months for its Digital Media segment’s Creative and Marketing Professionals customer group:

- Firefly continues to drive new user acquisition, with first-time Adobe subscribers growing more than 30% QoQ.

- Traffic to the Firefly App increased by over 30% QoQ, and paid subscriptions nearly doubled during the same period.

Firefly is Adobe’s “AI-assisted content ideation, creation and production” hub, with Adobe’s comprehensive family of commercially safe Firefly creative models and an expansive ecosystem of third-party models (including from Google, OpenAI and Black Forest Labs). Paired with Creative Cloud Apps, the Firefly App empowers creative professionals with enhanced precision and performance, ready to support them whenever and wherever inspiration strikes.”

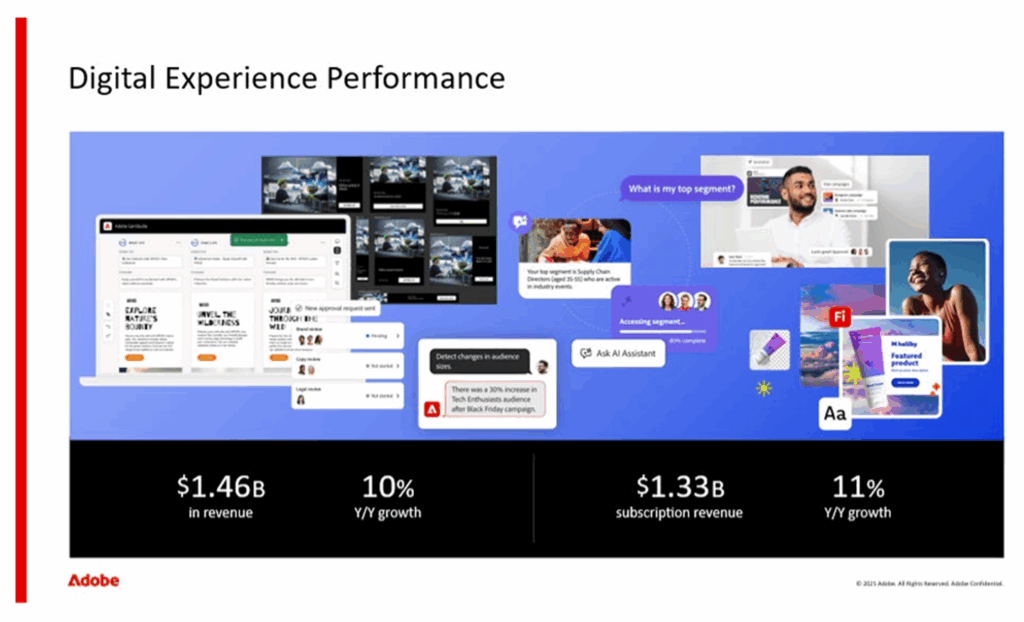

Digital Experience’s revenue increased 9.8% YoY to $1.46 billion. Subscription revenue during the quarter was $1.33 billion, reflecting an 11% YoY growth, positioning the company as a leading provider in its category:

- Adobe Experience Platform (AEP) and native apps saw strong demand, with Q2 subscription revenue increasing by over 40% YoY.

- GenStudio for Performance Marketing grew by over 45% QoQ.

- Sustained demand for Firefly Services and Custom Models as components of the GenStudio solution, leading to a 400% increase in annual recurring revenue (ARR) YoY.

Adobe’s Q2 FY2025 Earnings Report Income Statement

Revenue, $5.9 billion Q2 (+2.8% QoQ | +10.6% YoY) and $11.6 billion 6M (+10.4% YoY)

Cost of Revenue, $0.6 billion Q2 (+2.6% QoQ | +6.7% YoY) and $1.3 billion 6M (+6.1% YoY)

Gross profit, $5.2 billion Q2 (+2.8% QoQ | +11.1% YoY) and $10.3 billion 6M (+11.0% YoY)

Gross margin, 89.1% Q2 (+0.02% QoQ | +0.45% YoY) & 89.1% 6M (+0.51% YoY):

- Adobe’s Q2 gross margin of 89.1% surpasses that of most of its technology peers, based on recent earnings reports.

- For comparison, Intuit reported a gross margin of 81.5%, Salesforce reported 76.3%, Microsoft reported 70.2%, ServiceNow reported 78.9%, and Oracle reported 77%.

- Among the broader tech giants, Google (Alphabet) reported a gross margin of nearly 56%, Apple had a margin of 46.2%, and Amazon’s gross margin stood at around 48.7%.

- This puts Adobe at the very top of the group, underscoring the exceptional profitability of its subscription-based, software-driven business model.

Operating expenses, $3.1 billion Q2 (+6.7% QoQ | +10.6% YoY) and $6.1 billion 6M (-7.0% YoY):

- Research and Development (R&D), $1.08 billion Q2 (+5.5% QoQ | +9.9% YoY) and $2.1 billion 6M (+9.6% YoY).

- Moreover, R&D to Revenue ratio, 18.4% Q2 (+2.6% QoQ | -0.6% YoY) and 18.2% 6M (-0.7% YoY).

- Selling/marketing, and General and Administrative (SG&A), $2.0 billion Q2 (+7.6% QoQ | +11.3% YoY) and $3.9 billion 6M (+10.3% YoY).

- Additionally, the SG&A to Revenue ratio was 34.1% in Q2 (+4.7% QoQ | +0.6% YoY) and 33.4% for the 6M period (-0.1% YoY).

- Although Adobe’s operating expenses rose in Q2, the company’s 6M YoY operating expenses fell $0.46B, or 7%, primarily due to a $1 billion acquisition termination fee incurred in the first half of FY2024, which favoured the comparison.

Operating income, $2.1 billion Q2 (-2.5% QoQ | +11.9% YoY) and $4.3 billion 6M (+53% YoY):

- 6M YoY grew significantly, primarily due to a $1.15 billion 6M YoY growth (or +11.5%) in subscription revenue.

- Also, Q2 subscription revenue, $5.6 billion, represents +2.9% QoQ and +11.5% YoY growth.

- 6M YoY operating income benefited from the favourable comparison in operating expenses with FY2024 (no $1 billion acquisition termination fee dogging results).

Operating margin, 35.9% Q2 (-5.1% QoQ | +1.1% YoY) and 36.9% 6M (+38.5% YoY)

- Adobe’s Q2 GAAP operating margin of 35.9% is substantial, typically outpacing its peers in the application software sector.

- For comparison, Intuit’s recent operating margin was 35.0%, Salesforce reported 19.8%, and ServiceNow was 9.5%, while Microsoft stands out with 41.8%.

- Against broader tech peers, Adobe’s margin exceeds Amazon’s 10.7%, Alphabet’s 34%, and Apple’s 30.7%.

- The 6M YoY operating margin improved due to lower operating expenses compared to FY2024, which included a $1 billion acquisition termination fee.

Interest coverage ratio, 31.0 Q2 (-11.1% QoQ | -32.5% YoY) and 32.9 6M (-19.9% YoY)

Net income, $1.7 billion Q2 (-6.6% QoQ | +7.5% YoY) and $3.5 billion 6M (+59.6% YoY)

- The 6M YoY net income improved due to lower operating expenses in FY2024, as there was no $1 billion acquisition termination fee.

Net margin, 28.8% Q2 (-9.2% QoQ | -2.8% YoY) and 30.2% 6M (+44.6% YoY)

- Adobe’s Q2 GAAP net margin of 28.8% is exceptional, often surpassing most application software peers.

- For comparison, Intuit’s recent net margin was 27.8%, Salesforce reported 15.5%, ServiceNow had around 10%, while Microsoft distinguished itself with 35.8%.

- Adobe’s margin surpasses most of its larger technology peers, including Amazon at 8.1% and Apple at 23.2%, but trails Alphabet at 30.1%.

- The 6M YoY net margin improved due to lower operating expenses compared to FY2024, as there was no $1 billion acquisition termination fee.

Diluted EPS, $3.94 Q2 (+12.9% YoY) and $8.08 6M (+67.3% YoY)

- Adobe’s Q2 GAAP diluted EPS growth of 12.9% YoY reflects solid performance, but peers with stronger YoY improvements outpaced it.

- For comparison, Intuit’s 19.5% (tax and financial software strength), Salesforce’s 56.4% (strong AI and subscription growth), ServiceNow’s 19.0% (enterprise workflow demand), and Microsoft’s 14.6% (cloud and AI growth) all beat Adobe.

- Against broader tech peers, Adobe’s Q2 diluted EPS growth surpassed Apple’s -29.8% (weak iPhone sales), but trails Alphabet’s 30.9% (strong Google Services and Cloud performance) and Amazon’s 20.4% (AWS strength and cost efficiency).

- Adobe repurchased 8.6 million shares in Q2 FY2025 for $3.50 billion, leaving $10.90 billion of the $25 billion authorization from March 2024 remaining. Combined with its high net margin (28.8%) and aggressive share repurchase, Adobe’s high diluted EPS ($3.94 in Q2) amongst its peers is not surprising (Intuit at $2.63 in Q3 FY2025, Salesforce at $1.58 in Q1 FY2026, ServiceNow at $1.44 in Q1 FY2025, Microsoft at $3.37 in Q3 FY2025, Alpabet/Google at $2.20 in Q1 FY2025, Amazon at $1.53 in Q1 FY2025, and Apple at $1.53 in Q1 FY2025).

- Basic EPS, $3.95 Q2 (-4.8% QoQ | +12.9% YoY) and $8.1 6M (+66.7% YoY).

- Shares in Diluted EPS, 429 million Q2 (-2.0% QoQ | -4.8% YoY) and 433 million 6M (-4.6% YoY).

- Shares in Basic EPS, 428 million Q2 (-1.8% QoQ | -4.7% YoY) and 432 million 6M (-4.2% YoY).

Adobe’s Q2 FY2025 Earnings Report Balance Sheet

Cash/equivalents, $4.9B Q2 (-27.0% QoQ | -35.2% vs. FY2024)

- As mentioned earlier, Adobe repurchased 8.6 million shares in Q2 FY2025 for $3.5 billion (compared to $2.5 billion a year ago), which significantly impacted cash reserves. Compared to the 450 million outstanding shares at the end of FY2024 (November 29, 2024), Adobe has already taken 17 million shares off the market; 15.6 million through repurchases in Q1 & Q2 of FY2025. Additionally, the company has $10.90 billion remaining from the $25 billion authorization it received in March 2024.

- Adobe’s last twelve months (LTM) free cash flow was $9.4 billion, while LTM share repurchases totalled $12.3 billion. This suggests that Adobe is spending beyond its free cash flow on buybacks, thereby directly reducing its cash and equivalents.

- Cash generated from operations was $2.19 billion in Q2 FY2025, compared to $2.48 billion in the prior quarter. The decrease in operational cash flow contributed to the reduction in cash reserves, especially as expenditure (e.g., operating expenses $3.1 billion in Q2 FY2025 and investing $0.3 billion, or acquisitions) outpaced this cash generation.

- The earnings release did not mention any new acquisitions. Adobe’s ongoing investments in AI and partnerships (e.g., with Newell Brands for generative AI via Adobe Firefly and Adobe Express) suggest a focus on organic growth and strategic collaborations rather than acquisitions.

- The decline in cash and equivalents is primarily driven by aggressive share repurchases, potentially coupled with investments in AI and other strategic initiatives, as well as slightly lower operational cash flow compared to the prior quarter.

Current ratio, 0.99 Q2 (-16.2% QoQ | -6.9% vs. FY2024)

- Adobe’s current ratio is slightly less than 1.0, indicating that current liabilities are marginally higher than current assets. The primary reasons for this are high deferred revenue from subscriptions ($6.2 billion) and a reduced cash balance from $3.5 billion in share repurchases.

- For comparison, Intuit’s 1.60, Salesforce’s 1.42, ServiceNow’s 1.32, and Microsoft’s 1.25 all beat Adobe.

- Against broader tech peers, Adobe’s Q2 current ratio is higher than Apple’s 0.97, but trails Alphabet’s 1.42 and Amazon’s 1.08.

Total Debt-to-Equity, 1.46 Q2 (+13.0% QoQ | +27.3% vs. FY2024)

- Long-term Debt-to-Equity, 0.54 Q2 (+14.6% QoQ | +84.0% vs. FY2024)

- Total liabilities, $16.66 billion Q2 (-1.2% QoQ | +3.3% vs. FY2024)

- Long-term debt, $6.17 billion Q2 (+0.2% QoQ | +49.3% vs. FY2024)

- Shareholders’ equity, $11.4 billion Q2 (-12.6% QoQ | -18.8% vs. FY2024)

- On a quarterly basis, the long-term debt remained nearly flat, while the broader total liabilities fell marginally. However, the long-term debt increased by almost 50% compared to November 29, 2024, while total liabilities rose only slightly. Although the company did not engage in any notable borrowing in Q2, the impact of its borrowings in Q1 of FY2025 persisted.

- The aggressive share repurchase program (8.6 million shares in Q2 FY2025, following the 7 million shares repurchased in Q1 FY2025) reduces shareholders’ equity by removing shares from circulation. These share buybacks (to the tune of $3.5 billion in Q2) were financed using cash that could have otherwise bolstered shareholders’ equity.

- Further reducing shareholders’ equity is the fact that Q2 FY2025’s operating income of $2.19 billion was less than the amount spent on share buybacks. Moreover, operating income was 2.5% lower than Adobe reported in the first quarter of fiscal year 2025. So, cash reserves and debt covered the shortfall.

Adobe’s Q2 FY2025 Earnings Report Guidance

Q3 FY2025: Revenue expected at ~$5.9 billion, slightly above consensus ($5.88 billion). Non-GAAP EPS guidance of ~$5.10, in line with expectations.

Full-Year FY2025: Raised revenue guidance to $23.5–$23.6 billion (from $23.3–$23.55 billion), GAAP EPS of $16.30 to $16.50, and non-GAAP EPS of $20.50 to $20.70, reflecting confidence in sustained growth. Moreover, for FY2025, Adobe also targets:

- Digital Media segment revenue of $17.45 to $17.50 billion.

- Digital Media’s ending ARR book of business grew by 11.0% YoY.

- Digital Experience segment revenue of $5.80 to $5.90 billion.

- Digital Experience subscription revenue of $5.375 to $5.425 billion.

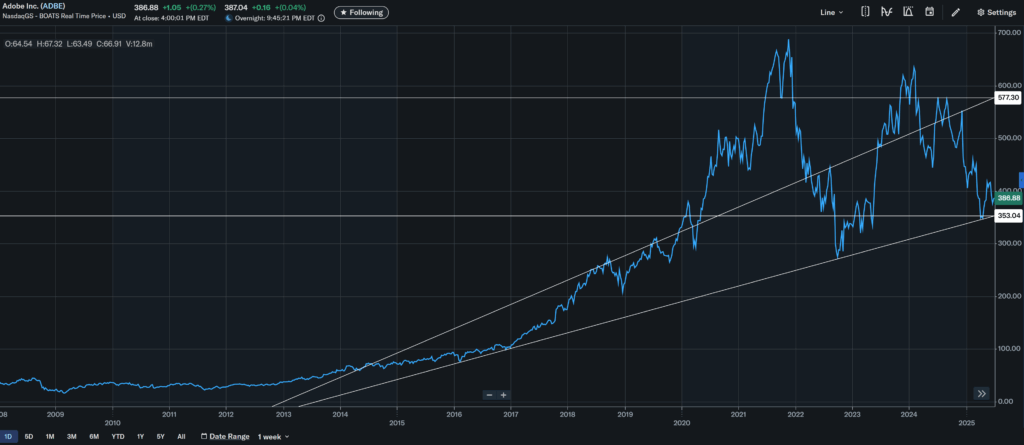

Stock Reaction: Despite exceeding forecasts and increasing its guidance, Adobe’s stock declined by approximately 7–9% following the release of its earnings report. This decline may be attributed to elevated expectations, concerns regarding cash consumption from stock repurchases, or broader market dynamics.

Adobe’s Q2 FY2025 Earnings Call Q&A Insights

- AI Monetization: Management discussed AI pricing strategies, highlighting that Firefly and other AI features are included in subscription plans, thereby creating opportunities for upselling rather than relying on standalone pricing models. They emphasized the potential for long-term Annual Recurring Revenue (ARR) growth from increased AI adoption.

- Competition: Adobe confidently addressed questions about competition from open-source AI or rivals like Canva by highlighting Adobe’s differentiated offerings, proprietary data, commercial safety, and enterprise trust.

- Share Buybacks: Management justified the substantial $3.5 billion repurchase in the second quarter, indicating it demonstrates confidence in long-term value creation. However, some analysts have raised concerns regarding the potential impact on cash reserves.

- Macro Environment: Adobe observed continued resilience in enterprise spending despite prevailing economic uncertainties, supported by robust retention rates and multi-year contracts that have strengthened their remaining performance obligations (RPO).

- Regulatory Considerations: Although no new regulatory issues were identified, previous scrutiny, such as that related to the Figma acquisition, was noted as an element in strategic planning.

Impact of Q2 FY2025 Earnings Report on Bull and Bear Theses

Bull Thesis Impact

The earnings report bolsters the bull thesis by showcasing Adobe’s ability to exceed expectations, raise guidance, and drive AI innovation. The stock’s post-earnings dip appears driven by market sentiment rather than fundamental weaknesses, presenting a potential buying opportunity for long-term investors.

- Strengthened by Financial Performance: The 11% year-over-year revenue growth, $5.06 earnings per share beat (non-GAAP), and revised FY2025 guidance significantly bolster the bullish perspective. The 12% increase in Digital Media Annual Recurring Revenue and the 10% rise in Remaining Performance Obligation illustrate strong demand and revenue visibility, further validating Adobe’s recurring revenue model.

- AI Leadership Validated: The earnings call emphasized Firefly’s commercial traction and enterprise adoption (e.g., Newell Brands), aligning with the bull thesis of Adobe’s AI-driven growth. Management’s confidence in embedding AI within existing subscriptions suggests a sustainable approach to monetization that does not disrupt customer retention.

- Enterprise Momentum: The 10% growth in Digital Experience and strong RPO growth highlight Adobe’s ability to capture enterprise demand, supporting the bull case for market expansion.

- Share Buybacks: The $3.5 billion Q2 repurchase aligns with the bull case of shareholder value creation, as it reduces the share count and could boost future EPS, despite short-term cash concerns.

Bear Thesis Impact

The earnings report provides ammunition to bears, given the cash burn from aggressive buybacks and the stock’s post-earnings decline, which highlights valuation sensitivity. However, the lack of new regulatory or competitive setbacks limits the immediate impact of the bear case.

- Cash Burn Concerns Amplified: The decline in cash reserves, driven by aggressive share repurchases that exceed free cash flow, strengthens the bear case. Investors may worry about Adobe’s ability to fund future acquisitions and research and development, especially in a competitive AI landscape.

- Stock Reaction Highlights Valuation Risks: The 7–9% stock drop, despite a beat-and-raise quarter, suggests that investors are pricing in lofty expectations or skepticism about near-term catalysts, supporting the bear case that the stock is overvalued.

- Competitive and Regulatory Questions Persist: While Adobe addressed competition in the earnings call, the lack of detailed AI monetization metrics or clarity on countering low-cost rivals (e.g., Canva) may fuel bearish concerns. Regulatory risks, though not emphasized in Q2, remain a background concern given past scrutiny.

- Cash Flow Decline: The drop in operating cash flow to $2.19 billion from $2.48 billion in Q1 raises questions about sustainability if expenditures (e.g., buybacks, AI investments) continue to outpace cash generation.

Putting It All Together

The Q2 FY2025 earnings report strongly supports a positive outlook for Adobe. The company achieved record revenue, exceeded EPS expectations, provided an upward revision of its guidance, and demonstrated AI-driven growth, all of which highlight its market leadership and operational prowess. With a 12% increase in Digital Media ARR and a 10% rise in RPO, Adobe shows strong demand and promising future revenue potential. Additionally, the ongoing adoption of Experience Cloud and Firefly by enterprises bolsters Adobe’s competitive advantage. The confidence expressed during the earnings call regarding AI monetization and enterprise retention further substantiates the optimistic perspective.

The bear thesis is strengthened by the substantial cash outflow resulting from share repurchases, which decreased cash reserves and contributed to the rise in the debt-to-equity ratio. The stock’s 7–9% decline indicates investor concerns regarding valuation or the absence of a significant catalyst, such as a major acquisition or more transparent AI revenue metrics. While competitive pressures and potential macroeconomic risks persist, Adobe’s stability in enterprise spending and unique AI offerings mitigate these issues.

Adobe’s earnings report supports its long-term growth, especially for those optimistic about AI and recurring revenue. While critics may highlight cash flow and valuation risks, these seem minor compared to Adobe’s core strengths. Investors should watch upcoming quarters for updates on AI profit and cash management.